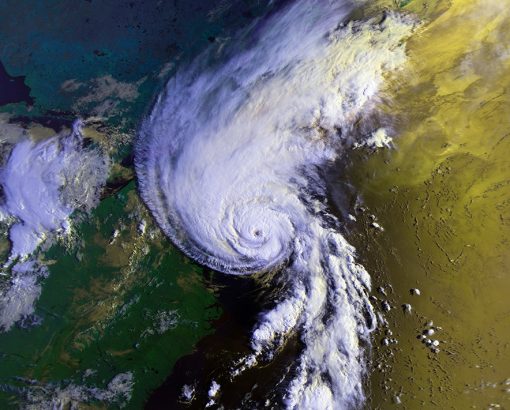

This past week, Floridians braced for the impact of a near category five hurricane as Ian’s 155mph wind path made landfall in southwest Florida on Wednesday. The long-term effects of Hurricane Ian are unclear, but immediate results indicate a battered Florida peninsula as noted by excessive flooding, storm surge, and high winds.

On an annual basis, sunshine state residents use the months of June to November to plan for catastrophic storms. That being said, the last significant hurricane to hit Florida was Irma in 2017. And even though hurricanes do not hit Florida every year, the residual fallout of Irma is still evident five years later with ongoing insurance claims and litigation.

Shifting to New England, natural disasters such as hurricanes are not as evident, but major winter storms, blizzards, nor’easters, and even wildfires or hurricanes can have widespread repercussions.

The takeaway here is that, although devastating natural disasters can be relatively uncommon, the results can be catastrophic and no region is immune. Natural disasters can have overwhelming effects on various communities, and inevitably include community associations. In both Florida and New England, condominium and homeowner associations should prophylactically consider the possibility of storms, wildfires, tornadoes, water issues from hurricanes/coastal occurrences, floods, blizzards, and extensive power outages.

But what exactly is a community association to do when these natural disasters occur? Importantly, condominium/HOA boards and property managers should both proactively and reactively implement systems and procedures to mitigate the ultimate risks, as well as understand who will bear the costs in the event of a natural disaster.

The effects of a natural disaster can be taxing on a community association due to the physical effects to property, economic impact, and potential emotional toll on a society. In order to lower the stress of dealing with a natural disaster, associations should formulate a risk management plan before a disaster strikes.

Sufficient Insurance: It is good practice for your community association’s insurance plan to include disaster coverage. This could include specific disasters such as flooding insurance or general disaster coverage. In any event, associations should examine the insurance plan to see that it will have the ability to cover replacement costs and payments that may need to be made to lenders. Encouraging unit owners to seek their own adequate homeowners’ insurance may be fruitful, especially for areas that the association is not responsible for. Understanding the claims’ process will also be important post-loss. Generally, after damages have occurred and the association submits a claim, the carrier will make a coverage determination as to whether the damages are covered or not. The board will then need to determine whether to settle the claim or retain public adjusters/counsel to seek further indemnification.

Ability to Pay Assessments: Another good proactive measure for a community association is to maintain an ability to pay assessments after a disaster strikes with proper budgeting mechanisms. Thoroughly examining the economic health and fiscal soundness of the community association through a reserve study is essential. The analysis of the association’s financial health may include adequate funding through not only reserves, but also obtaining appropriate loans or a line of credit.

Amending Governing Documents: As a general rule, community associations should try to ensure the governing documents are always up to date. To account for natural disasters, it may be a good idea for your community association to include language to account for potential disasters and who will bear the risks and be held accountable for payments. Additionally, community associations that are in different geographic regions may include different clauses. For example, if your community association is in a flood zone, the governing documents (and insurance coverage) could include extra information regarding what the community association will do if a flood occurs. For a community in New England, verbiage in the governing documents/insurance policies related to snowstorms may be included, but will be omitted from Florida’s documents.

Disaster Plan Committee: It is good practice to sub-divide a board to address certain categories, and that is no different when compiling a defined disaster plan, which will help streamline information to and from unit owners. For example, many Florida counties mandated evacuation for Hurricane Ian. An association’s well-communicated disaster plan would include certain pre-evacuation requirements such as removal of any furniture from outdoor balconies at the unit owner’s property.

Risk vs. Reward: As discussed, the probability of a natural disaster is rare, but the effects can be catastrophic. While the timing is uncertain when a devastating event will occur, a disaster could strike at anytime and anywhere, almost always catching those involved off guard and left to pick up the pieces. A community association should attempt to identify and reduce risks as much as possible beforehand. Further, by considering the unforeseen circumstances before they occur, the parties will be better equipped to deal with the disaster. Of course, every potentially exposed factor cannot be safeguarded and by spending exorbitant costs on capital projects to alleviate any chance of risk may not be the most prudent decision. However, accounting for the possibility of a disaster and minimizing the chance of deleterious effects in a cost-effective manner may be a wise decision by the community association’s board.

Even with the most detailed preparedness, it can be challenging to account for every variable after a natural disaster occurs. If the proactive measures turn out to be insufficient, there are still actions a community association can take to minimize costs and still pick up the pieces.

Property Rehabilitation: After a community association’s property is struck by a natural disaster, the board should have a plan in place to rehabilitate the damage if everything is not covered. The board should implement a strategy to ascertain who will be held responsible for the damage to each distinct area. Economic soundness is crucial here and obtaining a loan or withdrawing from a line of credit may help mitigate the inevitable high costs, especially in the event the impact is catastrophic. Another important wrinkle here is ensuring the proper contracts are in place with architects, engineers, and general contractors to oversee and estimate costs of repair.

Temporary Payment Plans: What should a community association do if there is no income? As discussed above, it is good practice to ensure the community association is fiscally sound. However, sometimes this may not be possible. After a natural disaster, the community association could set up a temporary payment plan until the initial shock of the disaster dissipates.

Aid to Homeowners and Emergency Board Action: The bearer of risk usually falls on either the homeowner or the community association, but sometimes, the language in the agreement may lead to some confusion as to who is responsible. By specifically clarifying who is responsible for the direct payments or insurance coverage of certain incidents will reduce the likelihood of any ambiguities. In order to avoid disputes with homeowners, associations will want to make their position clear, consult with counsel, and communicate the potential scope of liability between the association and homeowners. To take it a step further, Florida Statute Section 718.1265 specifically grants certain emergency powers, which includes implementation of a disaster plan and mitigation or evacuation procedures. In the event members do not evacuate, an association’s board should document all correspondences with the subject homeowners to avoid possible liability in the event a non-complying unit owner pursues action against the association due to injury and/or property damage.

Ascertaining Extent of Damages: After a natural disaster occurs, it may be difficult to assess what damages were caused by the disaster and what may have occurred prior or separately. Having a maintenance plan in place to evaluate the condition of the common areas on a weekly or monthly basis could help pinpoint disaster-related damages. Including photographic or video proof of the before and after condition may also help assess the amount of damages. Considering retention of expert architects, engineers, and/or general contractors to review cause and origin of loss, as well as extent of damages, could assist with not only the repair process, but combating underpaid/unpaid insurance determinations.

Up Next...